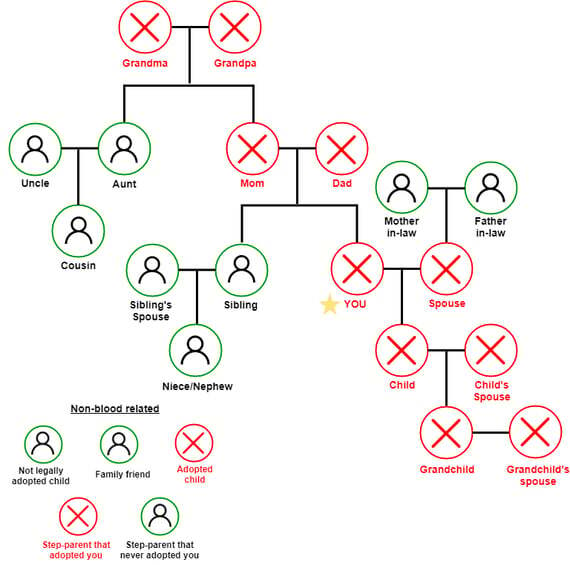

Self-Directed IRA Rules dictate that you cannot do business with a disqualified person like your parents, spouse, your children, your children's spouses... and companies where you or a disqualified person(see previous) owns 50% or more of the company. Review this family tree.

You are also a disqualified person.

Remember that you, or any family member, need to keep your IRA separate away from any conflicts of interest. Your IRA should only benefit from investments and business activity. You, or any family member, are not allowed to derive any personal benefit from investments or business activity in your IRA account(s).

Who is not a disqualified person in my family?

“Children” who were not legally adopted, aunts, uncles, nieces, nephews, cousins, in-laws, brothers, sisters, and non-blood-related family friends are not disqualified family members for prohibited transactions in IRA accounts.

What if a person changes in status through marriage?

If an individual’s status as a qualified or disqualified individual changes through marriage, It is wise to not continue doing business with that individual if it is via an investment or business relationship within a Self-Directed IRA. For example, you should not fund additional deals, add equity to a business owned by this individual, or invest in new deals with Self-Directed IRA dollars that are owned by this individual. If you want the investment to continue, you should not be change or negotiate new deal terms other than letting the deal reach maturity and exiting the investment. A "transaction" is defined as money entering or leaving an IRA or if deal terms are renegotiated.

If you want to be extra careful, you should maybe find a way to exit the transaction with that person before this concern happens.

Key persons at a company you own can be disqualified

Disqualified persons for your IRA own over 50% of a company, are the CEO, are an officer/director, or employees that own over 10% and are highly compensated can all be disqualified.

If other disqualified people, such as your children or spouse, own parts of the company, this counts in addition to your ownership towards the 50% threshold.

For example, if you owned 15% of a friend’s company and your children owned another 40%, that company and certain key persons would be disqualified from doing business with or receiving funds from your IRA.

Can I invest in the company I work at?

Why are these rules in place?

Generally, these laws are designed to prevent a person from attempting to avoid or unfairly reduce taxes.

The investment I want to make is associated with disqualified persons. How do I avoid a prohibited transaction?

You can aim to make an investment with someone who is not a disqualified person, or search for a similar investment opportunity that is free from a disqualified person's involvement. Doing business with a disqualified person puts your IRA at risk of a forced distribution and possible additional penalties from the IRS.

What are some of the possible penalties of a prohibited transaction?

-

Forced distribution of the IRA or Roth IRA.

-

Early withdrawal penalties if you are below age 59 and 1/2, which is typically 10% plus ordinary income taxes owed for IRAs.

-

Negating all of your investment gains in a Roth IRA due to disqualification of the investment and the associated Roth IRA tax treatment.

-

The IRS may assign excise taxes of up to 15% for the amount involved for an error that was created unintentionally, which can increase to a full distribution if the prohibited transaction is not fixed promptly.

-

The IRS may also assign excise taxes to Solo 401(k)s of up to 15%, which can increase to a full distribution if the prohibited transaction is not fixed promptly.

Was this article helpful?

Please sign in to leave a comment.