As of January 2024, Rocket Dollar began selling an IRA with a Trust to achieve checkbook control rather than a Colorado LLC. This was in response to feedback from California customers and investors, where high LLC taxes can be charged, and in response to increased reporting requirements for LLC beneficial owners.

This article is specifically about checkbook control. If you would like to see the pros and cons between checkbook control IRAs and Direct Custody IRAs, please review this article.

How is checkbook control different from normal retirement and trading platforms?

Checkbook IRAs funnel all IRA investment ownership through one entity, usually a Trust or LLC, so that the client can control all funds disbursements and investment returns through that entity.

As the trustee, you will have more freedom to move money, and also more responsibility to monitor and avoid prohibited transactions.

Does everyone need checkbook control?

No. Rocket Dollar, as one of the first to make checkbook control more affordable, has found that checkbook control primarily benefits three types of clients.

Does everyone need checkbook control?

No. Rocket Dollar, as one of the first to make checkbook control more affordable, has found that checkbook control primarily benefits three types of clients.

Those investing in individual real estate properties, where the investor must respond to numerous transactions throughout the year, as there is not a property management layer shielding the number of transactions. Those investing in real estate funds, syndications, multi-family partnerships, etc, will be just fine with a direct custody IRA. Some investors still target a checkbook control account as they must move on investments quickly or prefer a Solo 401(k) for its high contribution limits.

Do I need to have a physical checkbook in order to have "Checkbook Control?"

Our Gold IRAs that select an IRA Trust (Traditional or Roth) have access to a checking bank account, which has the ability to send money to almost any allowed investment. A physical checkbook is not necessary, but a nice way to send money from your IRA Trust’s checking account.

My investment issuer is asking me to contact Rocket Dollar for paperwork for my IRA. Where should I send them?

If you would prefer help and frequent communication with the IRA custodian, a Direct custody IRA might be better for you.

During the investment paperwork process, checkbook IRA clients do not need to check in with Rocket Dollar on paperwork. You, as the IRA trustee, will be able to sign the paperwork, with the name of your IRA Trust as the owner, and you signing as "Your Name, Trustee." You will put down the name of your trust, which defaults to your first initial and last name in the format JSMITH RD TR unless you ask our team for a custom name.

What are some of the advantages of the checkbook control model?

Pros:

- Recommended for sophisticated real estate investors who manage one or multiple properties, where a high level of transactions and billing are the direct concern of the IRA holder.

- Flexibility for advanced Cryptocurrency investors, custodial options

- Speed for high-volume private lenders, as transactions are logged as soon as the bank receives them and can be sent to new opportunities the same day or the next day.

- Have control of a bank account, checks, and debit card to manage investments.

- Easy to use for those familiar with an entity or business bank account

- No wait times for custodial approval, and can send a wire or check for same-day funding of an investment.

- Rocket Dollar creates the trust and introduces you to our partner bank.

Cons:

- Only available at our Gold service price level.

- Prohibited transaction screening falls completely on the investor. While a custodian of a direct custody IRA does not take responsibility for prohibited transactions, deal reviews can catch many basic prohibited transactions that could endanger the IRA of the account holder to distribution penalties.

- Requires active participation by the account holder to send money or share wire information to receive money back. Since the client is the only account manager on the bank account, the client must initiate all money movement. This level of self-management can frustrate those who wish to remain hands-off.

- Requires working with an additional entity.

- It takes longer to initially set up, at least two weeks with Rocket Dollar Gold or at least three weeks with Rocket Dollar Silver.

- Some investors are not familiar with Trust titling and investment trusts and prefer a simpler workflow and custodial oversight.

Why isn't checkbook control more popular?

Previously, the IRA LLC model was usually sold by lawyers or companies that would charge at least $1000 for setup, sometimes as high as $5,000. An investor might have to visit a lawyer, talk to a custodian to open an IRA, open their own LLC, and then find a bank that understood self-directed investing and wouldn't shut down or give them trouble over their account because it was not understood.

Rocket Dollar has been aiming to democratize access to the checkbook control model, which has become more and more popular for years as alternative investors want more control over their alternative retirement investments.

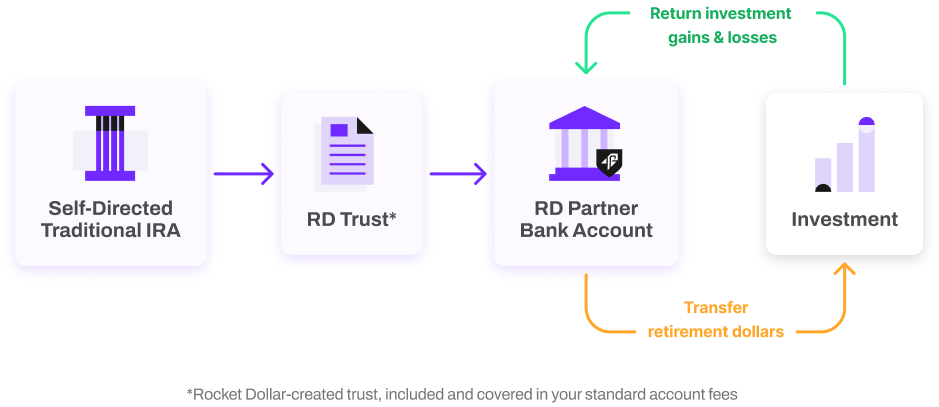

How do I get checkbook control with a Rocket Dollar Self-Directed IRA?

With a Trust IRA, we will provide you with the documentation needed to open and manage a Trust bank account linked to your IRA. From there, you will be able to make investments directly out of your account.

Money moves from the IRA>IRA Trust>Trust Bank Account. You can send the money to and from this bank account. You send money out to any investment you wish, then return capital, earnings, and related cash once you sell the investment, just as cash returns to your IRA from a stock or bond purchase

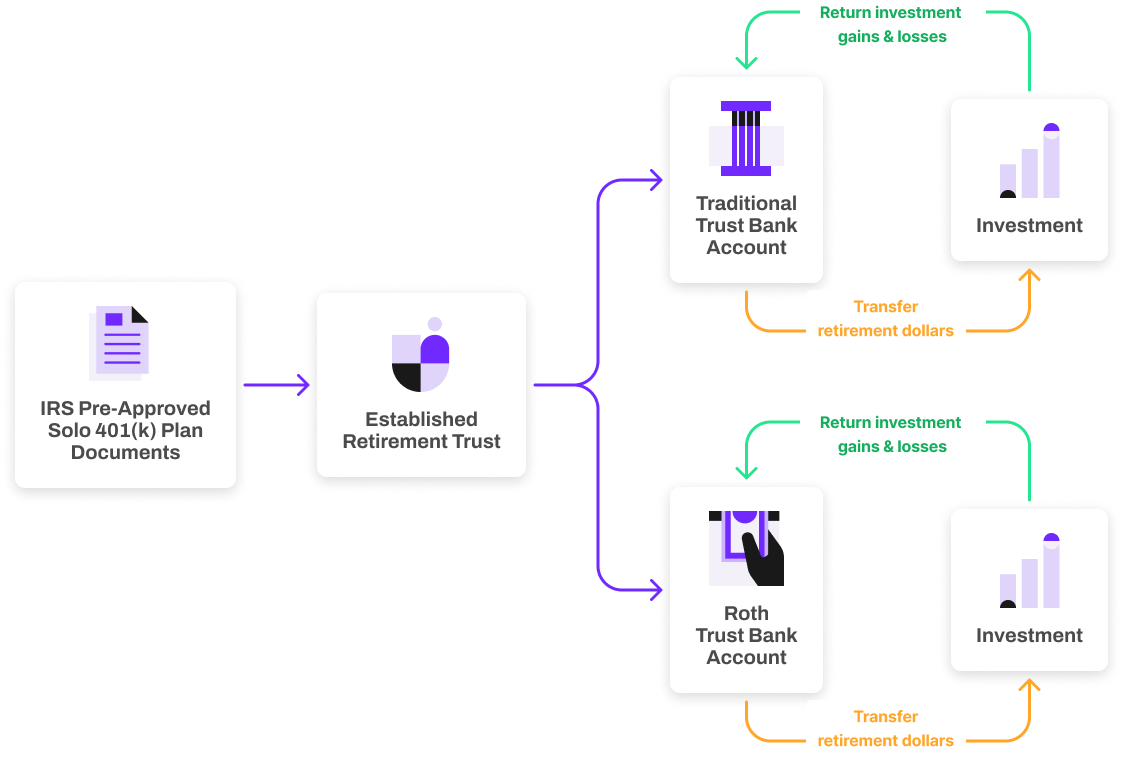

How do I get checkbook control with a Rocket Dollar Self-Directed Solo 401(k)?

For a Self-Directed Solo 401(k), we will provide you with the plan documents and EIN documents so you can go to the bank of your choice to open the appropriate number of trust accounts.

In most cases, you’ll need to open two bank accounts: one for pre-tax dollars and a second for Roth dollars. The Solo 401(k) plan establishes your retirement plan as a retirement trust. You will have checkbook control with each corresponding bank account. It’s important to keep pre-tax and Roth funds separate at all times.

Can I access publicly traded investments?

Our clients typically open a Fidelity-based trust account. Keep in mind, as this is not a standard Fidelity retirement account, the service is different. You will log in to Fidelity’s portal, and Rocket Dollar does not have a live technical connection to Fidelity.

When you are ready, you can purchase the shares directly from your Trust Bank account or the broker can open an /Entity/Trust trading account. You fund the trading account with your Rocket Dollar account and then report your tradable assets in our investment tracker.

Was this article helpful?

Article is closed for comments.